| Medical Practice Loan Options | |||||

|---|---|---|---|---|---|

| Loan type | Best for | Loan amounts | Repayment terms | Collateral required? | Approval time |

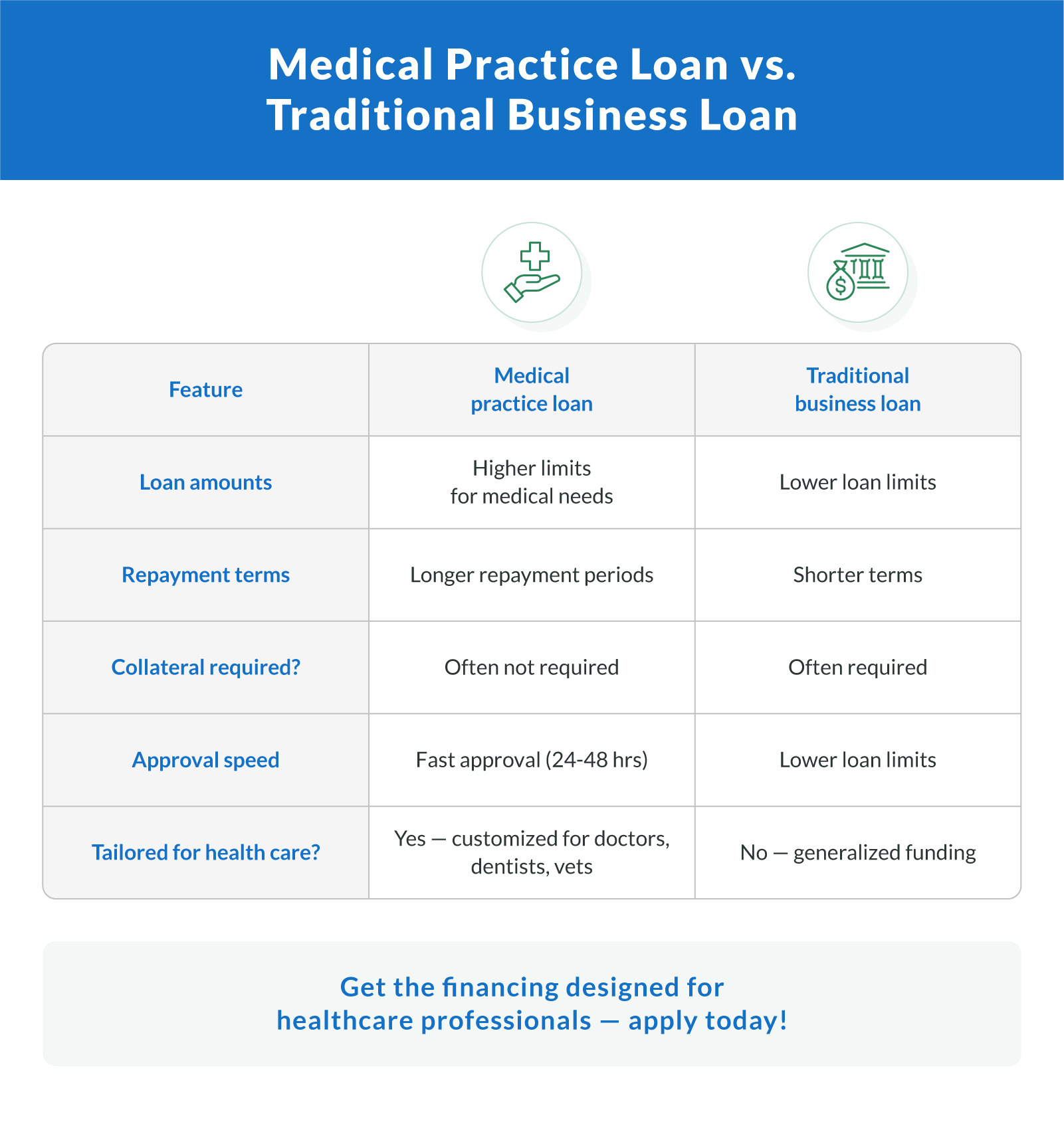

| Term loan | Growth, renovations | $10K–$5M | 6–60 months | No | 24–48 hours |

| Line of credit | Managing cash flow | $5K–$250K | Revolving | Sometimes (usually no) | Same day |

| Working capital loan | Covering day-to-day expenses, bridging reimbursement gaps | $10K – $500K | 3–24 months | No | 24–48 hours |

| Equipment financing | Buying diagnostic or surgical tools | Up to 100% cost | Based on equipment life | Equipment only | 24–72 hours |

| Invoice factoring | Accelerating insurance or payer receivables | Based on invoice value | Until invoices are paid | Invoices only | 24 hours |

| SBA 7(a) | Large expansion or acquisition | $50K–$5M | 5–25 years | Sometimes | Weeks to months |

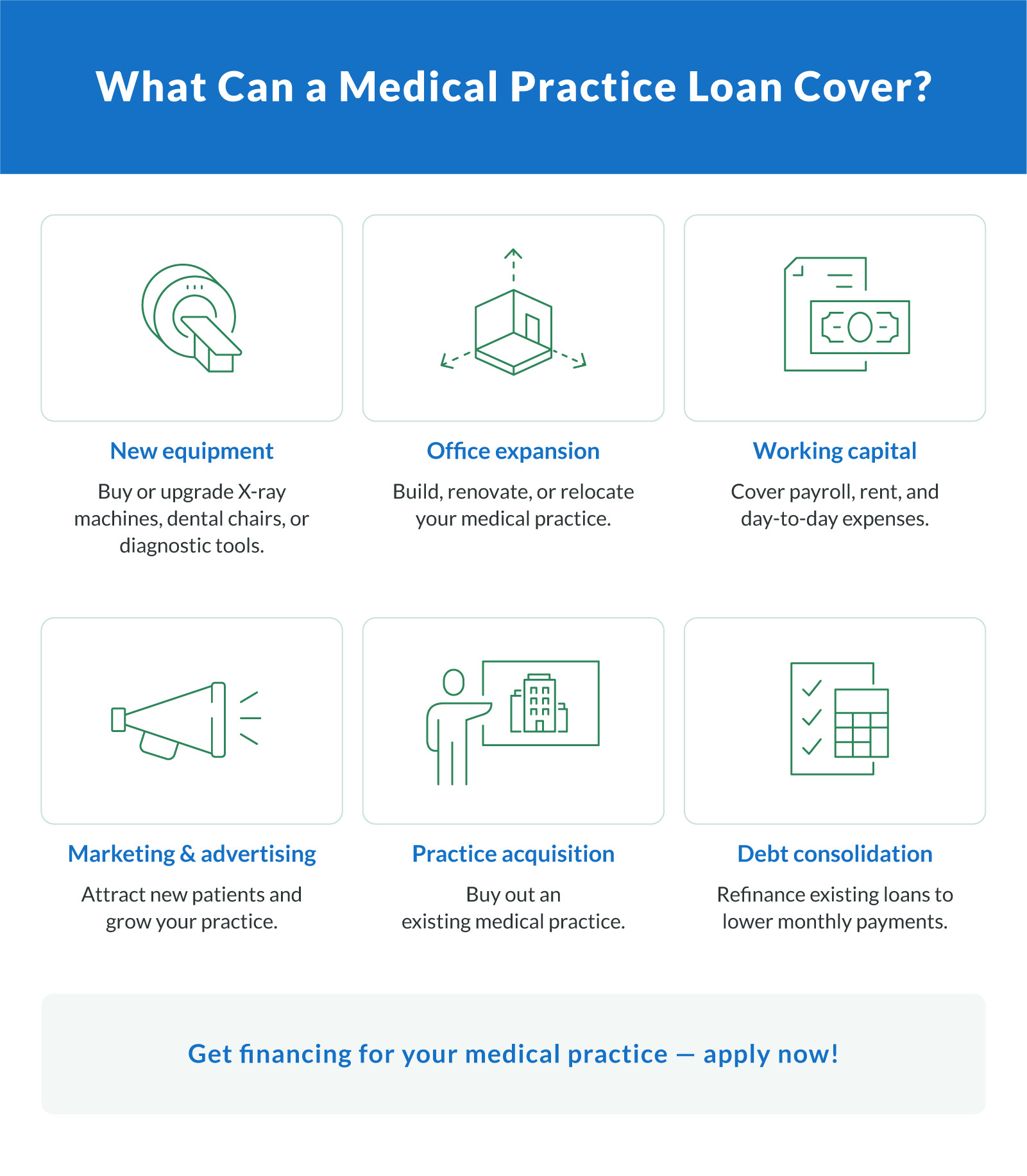

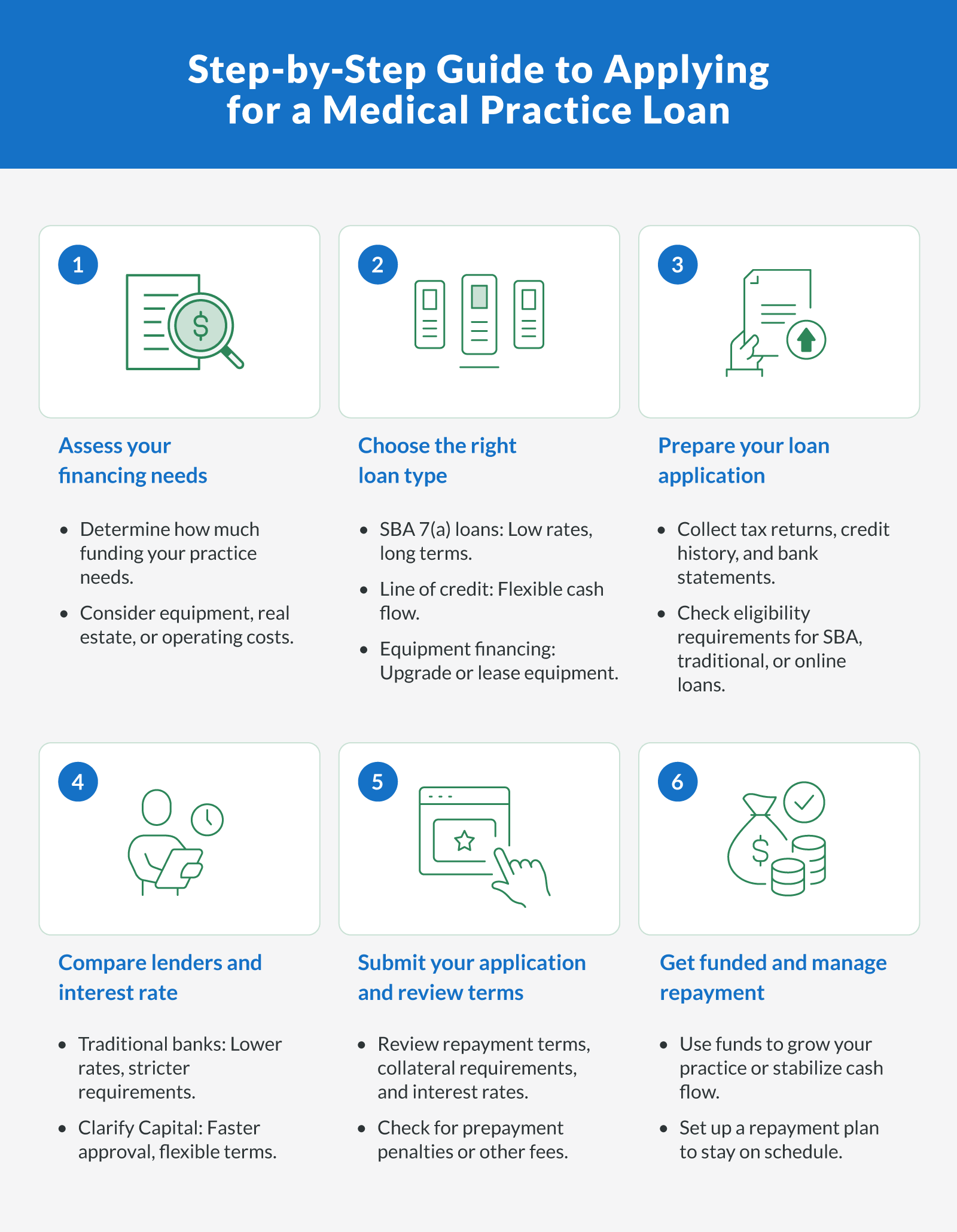

Do you need funds for new medical equipment or daily practice expenses? There are flexible loan options made just for medical professionals like you. You can get competitive rates and fast approval — sometimes in just 24 hours.

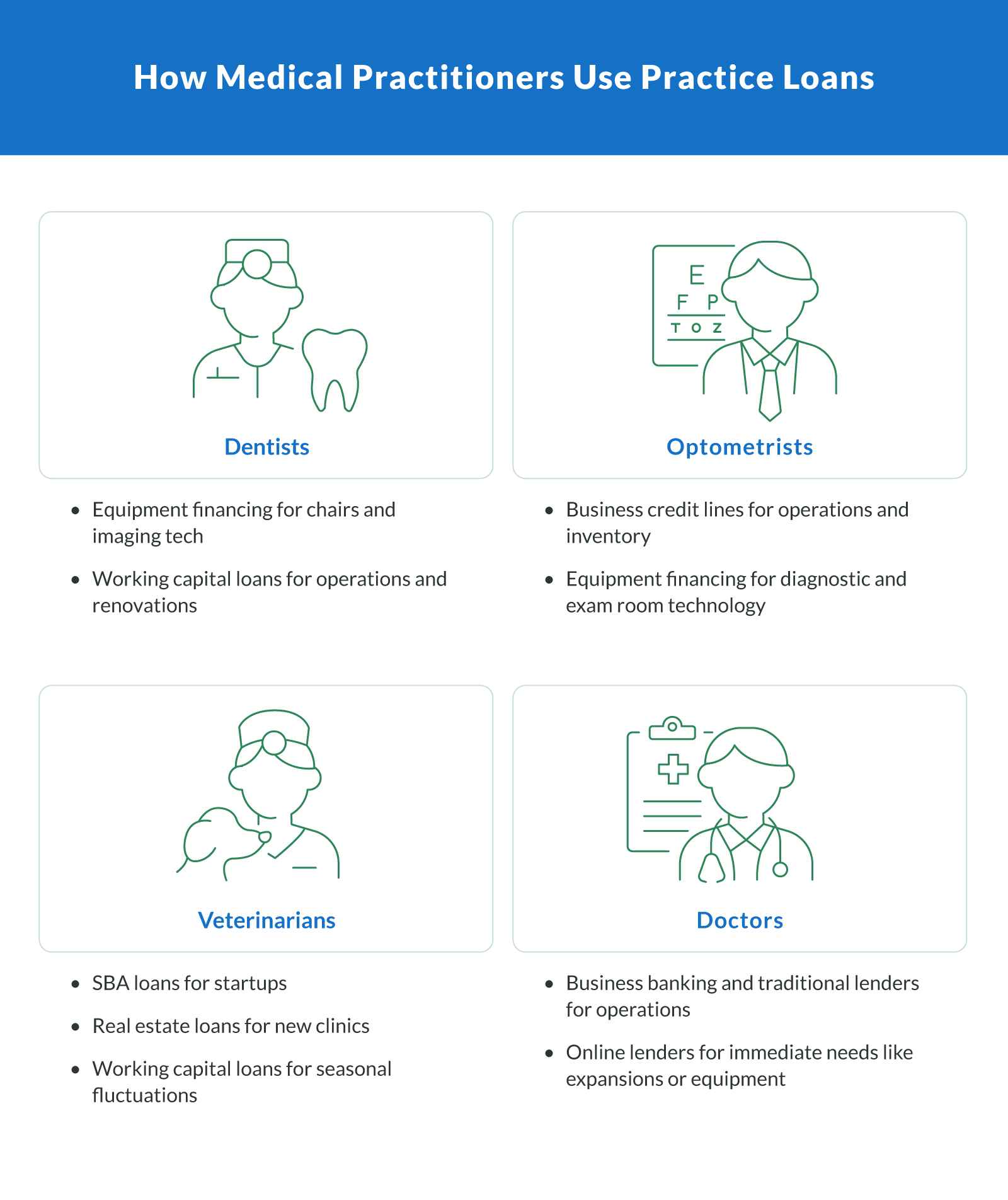

Medical practice loans are for providers like doctors, dentists, and veterinarians who want to grow or manage their business. Lenders often view health care professionals as strong borrowers due to steady income and long-term earning potential.

Finding the right loan takes time you don't have. That's why Clarify helps you compare offers in one place, without the stress. Our team works with you so you can choose what fits best and get back to running your practice.

To help you get started, we've outlined the most common types of medical practice loans, what they're best used for, and how they compare.

The 6 Best Medical Practice Loans for Doctors, Dentists, and Health Care Providers

Let's look at the best financing options for health care professionals. When you apply for physician loans through Clarify, your dedicated financial adviser will guide you through the process.

Term Loans for Doctors

When you think of business loans, you likely think of a term loan. A long- or short-term loan is structured similarly to traditional bank financing. You borrow a specific amount of capital at a specified APR and repayment terms. The duration of the loan term can be flexible based on your cash flow needs.

Here are the key benefits of term loans for medical practices:

Fast access to capital. These loans provide immediate funding to meet urgent financing needs and help you address time-sensitive opportunities.

Quick approval process. Credit approval and funding typically take only 24 to 48 hours, getting you the capital you need without lengthy delays.

No collateral is required. Unsecured term loans don't require collateral or a personal guarantee, reducing your risk while maintaining flexibility.

Flexible credit requirements. Lenders work with a range of credit profiles, including borrowers still building their credit history, making this option widely accessible for medical professionals.

Common use cases for term loans include:

Renovating a dental clinic to add new operatories for cosmetic or orthodontic services

Hiring additional staff at a chiropractic practice to support patient growth

Opening a second location for a veterinary practice in a nearby community

Business Line of Credit for Doctors

If you've ever had a home equity line of credit or used a business credit card, you already know the overall structure of a business line of credit. Lenders approve you for a maximum credit line, and you can withdraw funds as needed. You only pay interest on funds you use from the available credit line.

Here's why a line of credit might be right for your medical practice:

On-demand funding. You can withdraw funds as financial needs arise, offering the flexibility to manage varying expenses.

Pay for what you use. Interest is only charged on the amounts you withdraw, not your total credit limit, helping you control costs.

Build credit history. Using this credit responsibly can help improve your personal credit score over time, with lenders that report to personal or business credit bureaus, creating future financing opportunities.

Early payoff benefits. Most lenders in our network charge no prepayment penalty, allowing you to pay off the balance early without extra costs.

Common use cases for business lines of credit include:

Managing payroll gaps at a mental health or counseling practice during slow insurance reimbursement cycles

Purchasing short-term inventory for a dentist offering Invisalign or other orthodontic treatments

Covering emergency facility or equipment repairs at a physical therapy or rehabilitation clinic

Working Capital Loans for Medical Practices

Working capital loans provide short-term funding to help medical practices manage day-to-day expenses and revenue timing gaps. These loans are commonly used to stabilize cash flow during insurance reimbursement delays or periods of increased operating costs.

Here are the key benefits of working capital loans for medical practices:

Fast funding. Working capital loans are designed for speed, with approval and funding often completed within 24 to 48 hours.

Flexible use of funds. Loan proceeds can be used for payroll, rent, supplies, or other operating expenses without restrictions.

Minimal requirements. Many working capital loans are unsecured and rely primarily on business revenue rather than collateral.

Shorter repayment terms. Faster repayment schedules help practices address temporary needs without long-term debt commitments.

Common use cases for working capital loans include:

Covering payroll and overhead while waiting for insurance reimbursements

Managing seasonal fluctuations at a primary care or specialty practice

Paying vendors, suppliers, or lab costs during high-expense periods

Medical Equipment Loans

Medical equipment is the foundation of a successful practice. Aging technology can hamper your ability to provide quality care. Whether you are purchasing new equipment or are paying to repair existing ones, equipment financing can cover up to 100% of the costs, depending on creditworthiness and equipment type.

The structure of an equipment loan is similar to a car loan; the equipment, such as an X-ray machine, serves as collateral for the financing.

Here's what makes equipment loans an attractive option for medical practices:

Streamlined process. This financing option offers quick funding with minimal documentation required, simplifying the loan process.

Flexible credit requirements. Because the equipment serves as collateral, lenders can work with a wider range of credit profiles than unsecured loans.

Competitive rates. These loans typically come with competitive interest rates, making them a cost-effective choice for your practice.

Common use cases for medical equipment loans include:

Buying a digital X-ray or ultrasound machine for a veterinary surgical center

Upgrading chiropractic adjustment tables, laser therapy devices, or rehabilitation equipment

Installing new sterilization systems, imaging tools, or exam chairs in a dental office

Invoice Factoring for Health Care Providers

Invoice factoring allows medical practices to access cash tied up in outstanding invoices. Instead of waiting weeks or months for payment from insurers or other payers, practices can sell unpaid invoices to a factoring company for immediate funds.

Here are the key benefits of invoice factoring for medical practices:

Improved cash flow. Factoring converts unpaid invoices into working capital, helping practices maintain consistent operations.

No traditional loan required. Approval is based on the quality of invoices, not credit score or collateral.

Faster access to funds. Practices can receive cash in as little as 24 hours after invoices are approved, and depending on the factoring company and invoice verification process.

Scalable financing. As billing volume increases, available funding grows alongside it.

Common use cases for invoice factoring include:

Managing long insurance reimbursement cycles at multi-provider practices

Funding operations during periods of high accounts receivable

Stabilizing cash flow for practices with large payer mixes or delayed payments

SBA 7(a) Loan for Doctors

In cases where your working capital needs are further out into the future, an SBA 7(a) loan can provide some of the best interest rates and terms. SBA loans are secured partly by the U.S. Small Business Administration (SBA).

Your actual loan is through an SBA-approved lender. The federal agency guarantees up to 85% of loans under $150,000 and 75% of loans over $150,000.

Here are the main advantages of SBA 7(a) loans for medical practices:

Extended terms. These loans offer long payment terms, with loan lengths ranging from five to 25 years, providing payment flexibility.

Affordable rates. They typically come with competitive interest rates, making them an affordable financing option for your practice.

Government backing. The SBA guarantees either 75% or 85% of the total loan amount to the lender, depending on the amount borrowed, reducing their risk and improving your approval odds.

Common use cases for SBA 7(a) loans include:

Acquiring an existing pediatric, family medicine, or internal medicine practice from a retiring physician

Launching a new physical therapy, optometry, or chiropractic clinic in an underserved area

Purchasing a building to house a growing dental or multi-specialty medical practice